Half-Year Review 2025

- Jul 16, 2025

- 16 min read

In the 1986 film “Ferris Bueller’s Day Off”, actor Ben Stein plays a high school economics teacher discussing the impact of the Smoot-Hawley tariffs of 1930. His monotone delivery, combined with the comedically disengaged reaction of the classroom have made it a famous scene; one which, given the subject matter, has once again been making the rounds as of late. Before becoming an actor and entertainer, Mr. Stein was already an accomplished attorney, economist, and political pundit, as well as a speechwriter for both the Nixon and Ford administrations. Interestingly, Ben Stein’s father, Herbert Stein, was himself a respected and accomplished economist, serving on the Council of Economic Advisers during the 1970s. Though far less well-known than his son, perhaps his greatest “claim to fame” may be what is now referred to as “Stein’s Law”, a simple axiom that states:

“If something cannot go on forever, it will stop.”

At the moment, we believe that this adage rings true for a number of factors which may well have sweeping implications for the state of global growth and markets both today and in the future. It goes without saying that a great deal has occurred in the first six months of 2025, and in many cases, we believe these events serve as reminders that we may well be in the midst of a significant paradigm shift as certain forces that, clearly unable to persist forever, are indeed stopping (or reversing).

To start, perhaps it would make sense to offer some brief thoughts on the ongoing drama around trade and tariffs that has persisted in fits and starts since April. In some respects, keeping track of these events on their own has been a full-time job in and of itself, yet at the end of the day, it is difficult to say where the U.S. will ultimately net out with any of its trading partners. It is our view that a “resolution”- insofar as one can be achieved here- may take far longer than many would expect, and the uncertainty around that has the potential to weigh upon sovereigns, corporates and households alike. That aside, one thing we believe can be said with perhaps some degree of certainty is that the era of globalization that roughly began in the mid-1980s is likely ending. In some respects, we can understand the distaste that has developed, especially in the West, for this paradigm, whether due to the anemic growth following the Global Financial Crisis or the significant supply chain vulnerabilities this system highlighted during the COVID-19 pandemic. These issues, in many respects, were becoming increasingly untenable. However, a move away from unfettered free trade does come with one significant cost: the deflationary tailwinds created by the free movement of goods, services and labor are likely to come to an end. While the spike in inflation in the years immediately following the pandemic may well be attributed to short term, “transitory” disruptions in global supply chains, the fact is a move away from this model likely translates to a sustained return of higher levels of inflation over the long term. While there was a plethora of additional factors that impacted the path of inflation over the entirety of the postwar era, one can see that the “Era of Globalization”, which we roughly peg at 1985-2020, saw markedly lower inflation than the 35 years prior:

Yet it is not just this “Era of Globalization” that is coming to an end, as it is not just trade relationships that appear to be shifting at the moment. From a geopolitical perspective, this same period was also one in which, despite an ascendant China, the U.S. was, for all intents and purposes, the world’s sole superpower. In this position, the U.S. not only provided much of the West with a substantial defense shield, but also offered this to the world at large, protecting many of the vital shipping lanes, waypoints, and resources that fostered an environment of free trade. While this certainly came at a cost, when compared to the Cold War era preceding it, the U.S., along with the world at large, was able to enjoy a fiscal “peace dividend” for much of the period from the mid-1980s to the early 2020s, even after taking into account the costs of the wars in Iraq and Afghanistan in the 2000s through 2010s.

However, we would note this “Pax Americana” was already showing signs it was not sustainable decades ago: the economic rise of China in the early 2000s was accompanied by increasing interventions on the world stage, not just in the South China Sea, but further afield, as the world’s second largest economy sought to build influence in regions like Africa and Latin America in order to secure resources to compound its growth. At the same time, Russia’s 35-year post-Soviet trajectory has seen that country transition from a fledgling democracy to a chaotic kleptocracy to an unquestionable autocracy, one with designs on also further expanding its global sphere of influence. While the 2022 invasion of Ukraine was a clear and obvious marker of this new antagonistic positioning, so too have been Russian interventions in Africa and, to a greater extent, the Middle East. We saw this not only through Moscow’s relationship with the now-deposed Assad regime in Syria, but also its increasingly close ties with Iran. Especially since the October 7 attacks in Israel and the resulting war in the Gaza Strip, many are of the view that Iran’s support of any number of destabilizing proxies in the Middle East represents a threat, one that is likely coming with, at the very least implicit, if not explicit, support of Russia.

Leaving aside the fact that we have drastically oversimplified a complex set of geopolitical concerns here for the sake of brevity, what is important to know is that we are of the view that there is likely another paradigm shift occurring in global affairs: the stable, unipolar world in which we lived from the late 1980s to the 2010s is likely giving way to a more volatile, multipolar one marked by increased hostility and conflict. The implications of such a shift go far beyond troubling footage you may see from any news outlet, but could impact demand for raw materials, technology and other resources, and create a new set of demands for many of the major economies of the world. Many of these economies, already strained by massive debt burdens, may be required to significantly increase spending on defense. Europe has long been noted as a laggard on this front, an issue that Washington has increasingly highlighted in discussions with the leaders of the Old Continent. That said, there appears to be a significant shift in tone as of late, especially following elections in Germany in February, with the new government making defense spending a far greater priority than in the past. While Germany, with relatively low debt levels, likely has the fiscal room to engage in such spending, the fact is that much of the region now sees it has no choice but to increase defense expenditures, already-strained sovereign balance sheets notwithstanding.

These costs, however, will not be shouldered by Europe alone, as evidenced by increased spending by the U.S. itself. Indeed, with the passage of the Big Beautiful Bill in early July, the U.S. will be on track to have a $1 trillion dollar defense budget for the first time ever. For reference, this budget was “only” $600 billion a mere decade ago. While this is likely quite necessary given the shifting situation we have discussed heretofore, this is but one facet of a larger issue facing the world’s largest economy: the sustainability of the U.S. debt load. As things stand currently, U.S. federal public debt to GDP sits at 120.9%, more than twice what it was at the turn of the century. In recent letters, we have discussed the issue of U.S. government debt and its long-term economic implications. Regardless of one’s political persuasion, we would again reiterate that it seems the only bipartisan initiative in Washington today is raising the country’s debt load. We also feel it again worth noting that, while we are not necessarily predicting an imminent crisis in the market for U.S. government debt, the fact of the matter is that the current trajectory, at least in the long run, strikes us as unsustainable. Here again, “if something cannot go on forever, it will stop”. Volatility in U.S. rates markets has spiked a number of times in the past several years, most recently in wake of the “Liberation Day” tariff announcements in April. Though it has since moderated, the fact is that interest rate volatility, as measured by the ICE BofA MOVE Index, has been markedly higher in the post-pandemic era than it was in the years prior:

We believe that, through this elevated volatility, the market is likely trying to tell us something. While the post-GFC environment was marked by low interest rates, mild inflation and both implicit and explicit central bank support for risk assets, the world today and for the foreseeable future is likely to be quite different. Consider some of the factors we have discussed: waning (or even reversing) benefits from globalization, an increasingly unstable geopolitical situation and profligate fiscal policy by many of the world’s largest economies. All of these have the potential to further stoke inflation, or at the very least make it more volatile. This inflation volatility begets more volatility in rates markets, meaning that borrowing costs likely will remain elevated for quite some time, as investors seek additional compensation for the sheer uncertainty around the trajectory of inflation. Even when central banks cut rates in the face of any economic weakness in the future, it should be noted that these institutions (at least through conventional policy), can only dictate short-term rates. Longer-term rates, determined by markets, can (and often do) remain elevated in the face of a structurally inflationary environment.

These market-determined interest rates represent the baseline for the cost of capital for any borrower. As such, their level can impact the desire and ability to consume across the economy, from a company investing in a new factory to a consumer purchasing a new home or automobile. Said another way, interest rates, and by extension, the cost of capital, have a great deal of influence on economic activity, as well as the performance of risk assets. Consider the “stagflation” of the 1970s: as central banks sought to fight a persistent issue with inflation, with rates fluctuating significantly in the process, real GDP growth and the performance of U.S. equities left much to be desired. While we are not necessarily of the view that an outright redux of this period is in the offing, we do not discount the risk of a milder version of these conditions at some point in the future.

By contrast, we have seen several investors (and a great many speculators) attempt to make a more constructive case for the current backdrop. Though they frequently recognize the headwinds we have discussed, they suggest that the power of technology, especially that of artificial intelligence, is about to unleash a wave of productivity that will both promote growth and reduce inflation. While we would not deny for a second that there are likely significant positive economic benefits from harnessing the power of technologies like A.I., we believe there are several considerations that most investors have ignored. Few pay much attention to the notion that there is a great deal of energy and resource intensity required to both build and power the data infrastructure necessary to leverage A.I. at the scale envisioned, a difficult proposition in a world where inflation may run hotter than in the past. Similarly, the capital intensity of these projects may mean that elevated interest rates may hamper investments in the space at some point in time, creating a further constraint. While none of this means that A.I. will not see increasing usage throughout our world in time, realizing the full extent of its benefits may take a great deal longer than many wish to believe.

While we recently discussed the mismatch between investor expectations of A.I.’s benefits versus reality, perhaps it makes sense to revisit this on a more fundamental level. If one believes that the issues we have raised (deglobalization, geopolitical instability and fiscal challenges) threaten to cause inflation, and by extension, interest rates, to be elevated on a structural basis, one likely must rethink a great many of the better performing “trades” of the past few decades, and then consider how best to allocate capital in a world of several simultaneous paradigm shifts.

In a world that was marked by moderate inflation, low interest rates and geopolitical stability, the winning investment playbook, at least in retrospect, is somewhat clear. For us, it could best be represented by what is referred to as the “carry trade”. For those unfamiliar, a carry trade typically involves a strategy in which one borrows funds in a low-yielding currency and reinvests those proceeds in that of a higher-yielding one. While the carry trade itself traditionally refers specifically to foreign exchange trading, in our eyes, much of what has “worked” over the past several decades has followed a similar playbook: take advantage of cheap funding costs to provide leverage, reinvest the borrowed funds in higher yielding, typically riskier assets, and, assuming volatility remains muted, capture significant profits. Indeed, as rates fell lower and lower, one was best served by purchasing risk assets of any kind, ideally with leverage, knowing that volatility, save for a few brief spikes, was likely to be muted, preventing any major disruptions. Whether one was a buyer of bonds, equities or alternative assets, this framework was a useful one, especially in wake of the GFC as central banks around the world kept borrowing costs low and volatility muted.

One did not necessarily need to go out terribly far on the risk spectrum to see this in action. Consider the so-called “risk-free” asset, U.S. government bonds: If you purchased the iShares 20+ Year Treasury Bond ETF (Ticker: TLT) in July 2010 and held it until July 2020, you achieved an annualized return of 7.81% with income reinvested. While this is in our eyes an already attractive return given the risk/reward proposition, we would add that the opportunity to amplify this with leverage makes it even more so. We would note, however, that this long-dated U.S. Treasury fund has not performed as well since that time (offering a -9.09% annualized return in the 5 years from 1 July 2020). Yet again, we saw that “if something cannot go on forever, it will stop”: interest rates (and interest rate volatility) rose in the face of elevated inflation, making this seemingly safe asset much less so. While this has happened already in rates markets, we wonder what may be in the offing for riskier assets in the years ahead.

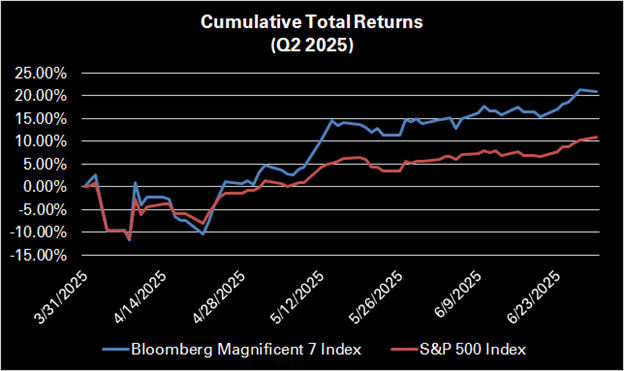

Equity markets have benefitted massively from a world of low inflation, low rates and low volatility. This has been particularly true for U.S. equities, especially large cap tech equities. In many ways, this stands to reason: low rates were able to fund the growth of innovative technology companies, whose undertakings held the promise of massive profits in the future. That investors may have to wait quite some time for said profits to be realized was not an issue, as the prospects for growth were considerable. Here again, we see the “carry trade” in action, leveraging low financing costs for the higher yield of long-dated growth. Little seems to have dented this narrative yet, as evidenced by the outsized recovery in the Magnificent 7 mega-cap U.S. tech stocks since April versus the broader market:

However, we frequently consider what could change about the world that may cause this trend to reverse. Interest rates have been elevated for some time now, yet this has done little to weigh on U.S. equity valuations, which remain elevated versus history. We would note markets seem to keep pricing in imminent rate cuts, with the timeline constantly moving forward in time. Should markets come to accept that this environment of elevated inflation and interest rates is not “transitory”, but rather now structural, we cannot help but wonder how equity markets may react. Once again, to be clear, this does not portend some sort of dramatic equity market rout, but rather a slow realization over time that weighs upon valuations.

Similarly, we wonder what other aspects of the paradigm shift discussed could do to U.S. equities over the long-term. Corporate America has benefitted massively from access to markets around the world, but fear that the impact of reduced global trade and increased geopolitical instability could hamper the performance of these businesses. Similarly, we worry about the prospects for U.S. risk assets in a world where relations between allies and rivals alike become increasingly strained. While the U.S. has been a natural home for capital from around the world for quite some time (see again: carry trade), we worry that the world in which we are entering may reduce foreign appetite for U.S. assets. Whether due to rising tensions or a deteriorating fiscal situation, foreign buyers may reduce their purchases of Treasuries, further pushing up yields in the process. The implications of higher rates could lead to a similar sell-off in riskier U.S. equities, again shifting the long-standing tailwinds for these assets in reverse. Here again, we should note that the timeline for such a scenario is long, but one we believe prudent investors should consider.

Perhaps nowhere has the implicit “carry trade” in risk assets of the past few decades been more evident than in the alternative investment space, particularly within private equity and credit. These asset classes have clearly benefitted from muted economic volatility and the free movement of goods, labor and capital around the world, combined with ever-cheaper financing to generate impressive returns, at least on paper. Yet here too, we believe that there are questions about how much longer this model can endure, as greater economic and market volatility raises financing costs and reduces liquidity. In a recent presentation that can be found here, we explore in depth the challenges facing alternative investments in this potentially shifting environment. While institutional investors long saw their outsized allocations to alternative investments as a means to enhance their portfolio performance, this perception appears to be shifting amidst these headwinds. Meanwhile, the alternative investment industry seems to be focusing a great deal of its attention on raising capital from individual investors lately, a development whose timing we will simply state is curious to say the least. While it is anyone’s guess how asset classes like private equity and credit will perform in the years ahead, we cannot help but wonder if many of the qualities that have made these asset classes so attractive in the past few decades may become liabilities.

Indeed, on a wider basis, we recognize that our dimmer outlook for many of these high performing asset classes and sectors is predicated on the notion that we are in the midst of a true paradigm shift, something that only time will ultimately prove out. While we believe we have outlined a fairly clear case for why the economic, geopolitical and fiscal ground may well be shifting under us, we have not yet discussed how we believe one may best position their portfolio accordingly. If the “carry trades” we have discussed are no longer going to work, what will?

Probably our most core view is that investors need to seek out assets which are valued in such a fashion that one is achieving a meaningful real return across the market cycle and doing so while keeping leverage to a minimum. We have discussed this in the past, but businesses whose success is not predicated on cheap financing and are either levered to inflation or have the pricing power to overcome it are likely to perform well in the forthcoming environment we have discussed. In a less stable world, seeking to acquire such assets at a discount provides an additional “margin of safety”, likely further enhancing returns, and making one’s immediate “yield” on their investment that much higher. This is especially attractive in a world where, given interest rates, cash actually generates an inflation-adjusted return, quite unlike what we have experienced for most of the post-GFC era. In sum, in a world that could be described as far less benign than in the past, asset quality matters a great deal more than it used to.

We recognize however that this abstract description of the “ideal assets” to own for the years ahead may be somewhat unsatisfying. However, looking at client portfolios, we believe you can see some key areas we believe continue to represent ignored opportunities. We own several resource-related businesses, both in the energy and mining spaces, which we believe will benefit from the often-overlooked material demands our world faces, and the inflation protection they thus provide. In addition, we seek to own businesses which can benefit from increased spending by sovereigns and corporates alike on improving infrastructure, both physical and digital, given the shifts we have discussed. While we made no major additions to client portfolios of this kind in the first half of the year, we have continued to watch and analyze a number of businesses that are levered to such trends, waiting to both build a confidence level and buy at what we see to be a fair price in light of the balance of risk and opportunity. Despite a volatile first half of 2025, we believe that owning these assets, in combination with our more cautious positioning overall, has been a meaningful benefit to client portfolios so far this year.

We would also note that client portfolios remain generally overweight non-U.S. equities, and this has likely been a tailwind as well of late. While we have noted the wide differential in valuations between U.S. and non-U.S. equities for some time now, we believe it interesting that markets have (finally) begun to take notice. At least partially, we view this as yet another manifestation of the paradigm shifts discussed, as investors seek to diversify their holdings away from the U.S.

Regardless of what may be driving this shift into international equities, the MSCI EAFE (in dollar terms) outperformed the S&P 500 by the widest margin of any half-year calendar period in the past 25 years:

While overseas markets have as a whole generated impressive returns, we remain particularly constructive on European equities, especially in the small and mid-cap space. While we have discussed many of the factors we find compelling about smaller businesses in the region in past letters, this is one area where investors have clearly taken notice. Consider the performance of our Focused European Value Strategy, which has returned 33.3% year-to-date for fee-paying accounts as of 30 June, outperforming the S&P 500 Index and the Nasdaq 100 by 27.8% and 25.3%, respectively. While six months of outperformance only says so much, we are of the view that this is a long-term investable theme and believe the portfolio companies within the strategy will benefit from many of the paradigm shifts we have discussed. If you are interested in learning more about our Focused European Value strategy, we highly recommend watching a webinar we recorded in March, or setting up a conversation with Zach, who has fronted our efforts investing in the region.

We recognize that, in contrast to many past letters which have focused on what has happened recently and what may lie ahead in the near term, this was a piece where we have made some rather strong prognostications about how the world may look in the years and decades ahead. Admitting that it will take as much time to find out whether these views aged well, we do believe that there is no shortage of signposts suggesting we may be on the right track. This may seem somewhat hard to believe at a time when U.S. equity markets are making new all-time highs, retail investors are pouring into high-flying technology companies and a plethora of new vehicles for speculation of all kinds are coming to market. If nothing else, we consider these to be signs of complacency around the notion that the market and economic conditions of the past few decades will last forever. Given the issues we have highlighted, we are anything but convinced.

As such, we believe that being prepared for significant paradigm shifts when it comes to the backdrop for inflation, rates and valuation of risk assets makes sense, and have positioned client portfolios accordingly. We would also note that, in the event that we are wrong, we believe that the quality of the assets we own, in combination with the valuations at which we own them, is likely to provide downside protection. We believe similar protection would be provided in the event of a major market dislocation, as evidenced by the performance of our client portfolios in the face of the post-Liberation Day market rout. Overall, regardless of what may lie ahead, whether tomorrow or in the years hence, we are confident in our positioning.

That said, if you are of the view that your portfolio does not align with your needs at this time, we believe setting up a time to connect with our team is more important than ever. At the same time, if you simply would like to explore in greater detail some of the views we have shared here and how they inform our investment process and portfolio construction, we would also encourage you to reach out- we welcome any and all opportunities for dialogue.

We very much appreciate your continued support and recognize the trust you put in our team. We wish you a relaxing, pleasant summer, and wish you all the best as we move into the back half of this year.

Comments